- Buy Crypto

- Markets

Futures

Futures- Spot

- Copy Trade

Earn

Earn- More

Week 14 On-Chain Data: Tariff Winds Intensify Market Chaos: Where Should Bitcoin Make Its Next Move?

Original Article Title: "Tariff Waves Intensify Market Chaos, On-Chain Signals Hard to Trust: Where Should Bitcoin Make Its Next Move? | WTR 4.14"

Original Source: WTR Research Institute

Weekly Recap

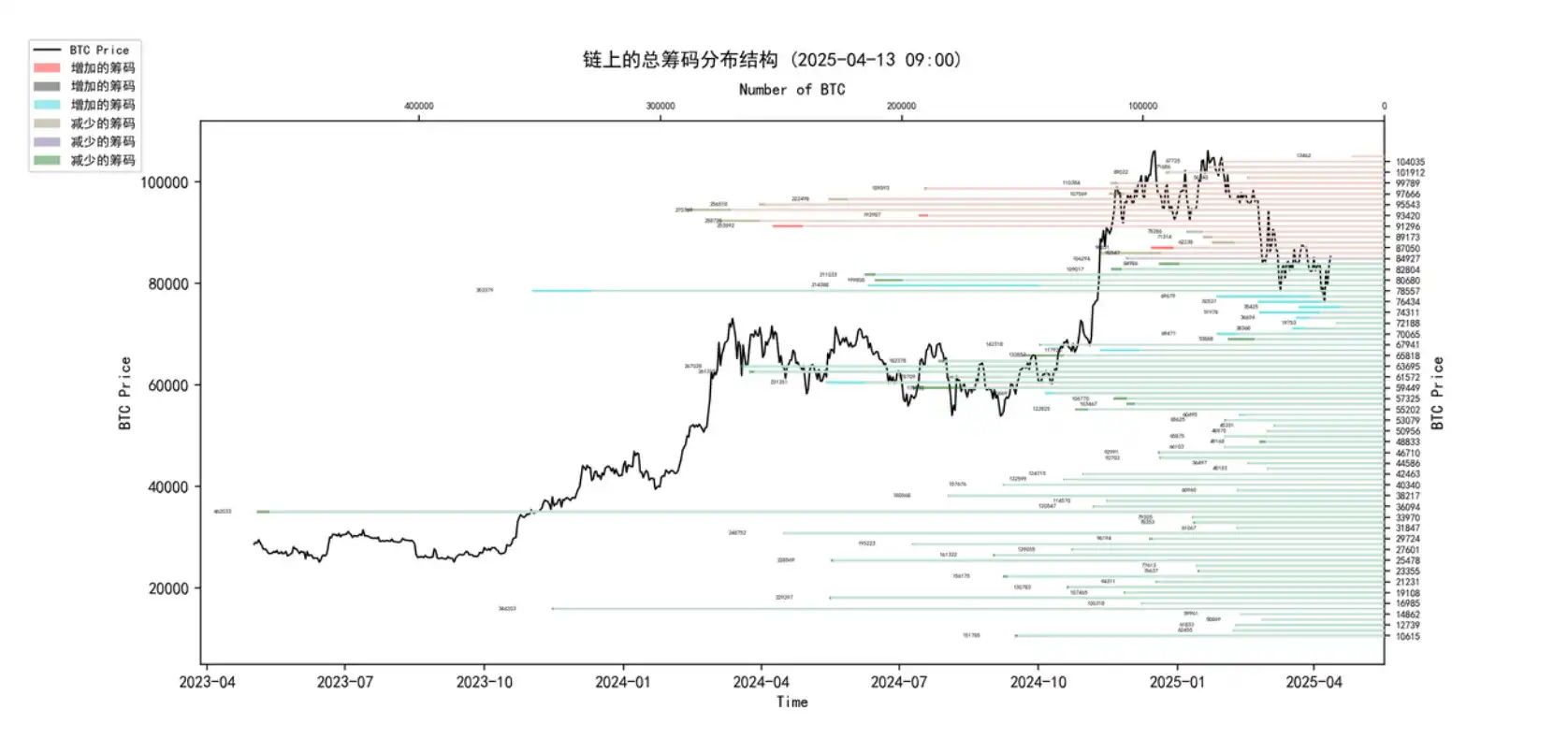

From April 7th to April 14th, Bitcoin reached a high near $86,100 and a low near $74,508, with a fluctuation range of approximately 15.56%.

Looking at the distribution of chips, a large number of chips were traded around 80,000, providing some support or resistance.

• Analysis:

1. 60000-68000: Approximately 1.51 million coins;

2. 76000-89000: Approximately 1.72 million coins;

3. 90000-100000: Approximately 1.99 million coins;

• The probability of not breaking below 70,000 to 75,000 in the short term is 70%;

• The probability of not breaking above 85,000 to 90,000 in the short term is 80%.

Key News Highlights

Economic News

• Goldman Sachs has raised its 2025 gold target price from $3,300/ounce to $3,700/ounce (a 12% increase).

• Fed Governor Waller believes that the high inflation caused by tariffs is temporary. In a scenario of small-scale tariffs, rate cuts may take place in the second half of the year. In a large-scale tariff scenario, if the economy significantly slows down, there may be a preference for earlier and larger rate cuts.

US Economic Data and Expectations:

• The New York Fed's 1-year inflation expectation for March in the US rose to 3.58% (higher than the expected 3.26% and previous value of 3.13%).

• The New York Fed expects the US unemployment rate in March to rise to the highest since April 2020.

• March CPI inflation fell to 2.4%. Tariff Policy and Its Impact:

• Over the weekend, Trump's tariff measures changed again, exempting some electronic products from "reciprocal tariffs."

• Economists believe the exemption was made due to the realization that the tariff shock and its resulting chain reaction touched a sore spot.

• Analysis suggests the exemption is a sign of US concessions, possibly under pressure from the bond market (the bond market is seen as Trump's top priority).

• Analyst James Van Straten believes that Trump's tariff uncertainty triggered a market sell-off starting on April 3rd.

• Fox reporter Charles Gasparino believes that the market's reaction to the "Tim Apple Tariff Exemption" will be positive and may boost the Nasdaq.

• Investors widely consider the tariff plan to be one of the worst policies in recent years. Trump's erratic tariff measures have shaken market confidence in U.S. policy and the economy.

U.S. Treasury Market:

• JPMorgan Chase CEO Jamie Dimon expressed readiness to deal with the turmoil in the nearly $30 trillion U.S. Treasury market, believing the Fed would only intervene during market panics.

• Last Friday, the U.S. Treasury market experienced a $29 trillion sell-off, marking the worst week of 2019.

• Looking back at March 2020, a U.S. Treasury market collapse forced the Fed to undertake trillions of dollars in bond purchases to intervene.

Economic Recession Concerns:

• BlackRock CEO Larry Fink warned that the U.S. economic recession may have already begun, with economic pressures and protectionist trade policies being key driving factors.

Market Focus and Outlook:

• Market focus may shift from tariff headwinds to rate cut expectations, signaling a potential change in market sentiment.

• Easing inflationary pressures could provide room for Fed rate cuts in the May and June meetings and relaxing financial conditions.

• Analysts are watching for when the Fed will intervene in the market.

Cryptocurrency Ecosystem News:

• U.S. Senator Tim Scott expects the Cryptocurrency Market Structure Act to become law by August 2025.

• The Senate Banking Committee advanced the Stablecoin Regulation Act "GENIUS Act" in March 2025, prioritizing crypto policy, emphasizing innovation over regulation to preserve U.S. leadership.

• SEC Acting Director Mark Uyeda indicated a consideration for establishing a short-term crypto regulatory framework to allow for innovation while developing a permanent solution to promote blockchain innovation.

Institutional and Corporate Developments:

• BlackRock's BUIDL Fund reached $2.372 billion in size, posting a 25.07% weekly gain.

• Tether CEO Paolo Ardoino stated a 13% increase in stablecoin users in Q1 2025.

• Japanese publicly traded company Metaplanet Inc. announced the acquisition of 319 BTC.

• MicroStrategy acquired $2.858 billion worth of BTC (equivalent to 3459 BTC) from April 7th to April 13th.

• Tether minted $1 billion in new stablecoins on April 12th.

Market Insights and Analysis:

• White House President's Working Group on Financial Markets Executive Director Bo Hines (as reported by Cointelegraph) indicated the need to accumulate BTC as soon as possible before it becomes more expensive.

• Analyst James Van Straten pointed out that the BTC/VIX ratio has touched a long-term trend line, historical data shows that this often precedes a BTC price bottom (prior effective time points: August 2024, March 2020, August 2015). If the support holds, BTC may have already established a long-term bottom.

• JPMorgan CEO Jamie Dimon believes that the turmoil in the U.S. bond market and subsequent Fed interventions may lead investors to turn to BTC as a hedge against currency instability (similar to the situation in 2020).

• Analysts believe that an economic slowdown may prompt the Fed to change its tightening policy, triggering new liquidity and becoming a major catalyst for BTC and other crypto assets.

• Looking back at March 2020 when the Fed intervened in the bond market, the crypto market also experienced a significant increase.

Long-Term Insight: Used to observe our long-term situation; Bull Market/Bear Market/Structural Changes/Neutral State

Medium-Term Exploration: Used to analyze the stage we are currently in, how long this stage will last, and what circumstances we will face

Short-Term Observation: Used to analyze short-term market conditions; as well as the emergence of certain directions and the likelihood of certain events under certain conditions

Long-Term Insight

• Holder Structure and Belief HODL Wave

• ETF's Structural Impact

• Illiquidity of Long-Term Whales

• Trading Platform Status of Major Whales

(Below Image Holder Structure and Belief HODL Wave)

After experiencing multiple market cycles, the group of long-term holders (LTH) continues to grow, constituting the market's "ballast."

Although some old coins (e.g., 2 y-5 y) have moved during price peaks (taking profits), those holding the oldest coins (e.g.,>5 y, purple area) have remained relatively stable and have even slightly thickened during recent consolidation. This indicates that the most steadfast long-term holders have not panicked and sold off due to recent fluctuations. Their holdings provide a solid underlying support for the market.

The core narrative of the HODL Wave Chart is the continuous maturation of supply. Over time, newly incoming supply (warm colors) gradually ages (turns into cool colors) and is absorbed by stronger-handed holders. The current period of consolidation, while putting pressure on short-term holders, also provides a time window for more Bitcoin to move from short-term holders to medium to long-term holders, setting the stage for a healthier uptrend in the future.

(Structural Impact of ETF in the Following Chart)

Although ETF inflows have weakened recently, the current slowdown in inflows can be seen as a normalization after the initial excitement and a reaction to the current macro uncertainties.

As long as the macro environment improves or new market catalysts emerge, the ETF channel could quickly become a significant source of incremental capital. Its mere existence enhances Bitcoin's maturity as an asset class and long-term appeal.

(Long-term Whales of Illiquidity in the Following Chart)

The Illiquid Supply Shock Ratio (ISSR) exhibits clear cyclical patterns. Historically, sustained ISSR growth (orange line rising, blue zone positive) has often accompanied the accumulation phase of a bull market. The current plateau period indicates that strong hodling momentum remains intact.

(Trading Platform Status of Large Whales in the Following Chart)

Intensifying Divergence, Not Unidirectional Selling: Current net inflows coexist with net outflows, reflecting the disagreements and complex maneuvers among major players (whales).

• On one hand, some early profit-takers or whales concerned about the macro picture are moving tokens to exchanges during rebounds (net inflows), exerting selling pressure.

• On the other hand, there are also whales actively withdrawing from exchanges during price pullbacks (net outflows), typically seen as bullish long-term accumulation behavior.

This divergence is likely to persist for some time. Clarification of the mid-term trend requires observation of which force predominates: continuous net inflows suppressing the price or net outflows beginning to dominate, indicating whales are reinitiating large-scale accumulation. Of course, even in the presence of short-term selling, whales accumulating at key support levels or when they believe the value is undervalued (net outflows) is a crucial prerequisite for the market to bottom out and start the next major uptrend.

Outlook:

On-chain data paints a picture of short-term volatility, medium-term significance, and long-term structural optimism:

• Short Term: The market is in a consolidation phase, ETF momentum is weakening, and divergent behavior among whales is leading to a tug of war between bulls and bears. Prices may continue to fluctuate or face a retracement risk. It is crucial to monitor macro-environmental changes and marginal improvements in on-chain supply-demand indicators.

• Medium Term: Whether the market can resume an uptrend depends on:

1. Favorable macro-environmental shifts (such as interest rate cuts);

2. Whether ETF fund flows can sustain continuous inflows;

3. Whether whales shift from divergence to net accumulation (continual net outflows from exchanges);

4. Whether illiquid whales are growing again;

5. Within the HODL wave, whether the supply can further mature, relieving pressure from short-term holders.

Therefore, while facing short-term challenges and volatility, from a medium to long-term perspective, as long as the core on-chain structure (such as LTH holdings, supply maturity) remains intact, and new demand-driving factors (potentially from macro improvements, continued ETF adoption, or new market narratives) emerge, the crypto market (especially Bitcoin) still has the potential for continued growth.

Medium-Term Exploration

• Whale Composite Score

• Short-Term Profit Percentage Composite Model

• VDD

• Price Structure Analysis at Various Levels

• Network Sentiment Positivity

(Whale Composite Score Chart Below)

Whales have been extensively involved in the market recently and are currently an important holding group within the ecosystem.

(Short-Term Profit Percentage Composite Model Chart Below)

The short-term profit structure remains relatively healthy, showing no signs of excessive profits in a stock environment (i.e., the green sell-off zone). The current participant issue may lie in the overall shift between positive and negative states. Relatively neutral, the tense macro environment is also continually shaping the boundaries of market participants' choices.

(VDD Chart Below)

The current area is still a holding area with relatively good risk-reward ratio. The selling pressure from high-weighted entities remains constrained within a specified range. As the process of gradually restoring the pricing model progresses on-chain, de-leveraging activities may become less frequent. This would be a relatively good holding position.

(See the Price Structure Analysis below)

In the short term, the market has gradually moved away from oversold levels (79,000), but the main issue currently on-chain is not the selling pressure. It is instead the sustained buying power and the level of liquidity recovery.

(See Network Sentiment below)

The network sentiment has been fluctuating, oscillating between positive and negative. In a tense gaming environment, on-chain participants also appear indecisive overall. From a liquidity perspective, a consistent direction has not yet emerged.

Short-Term Observations

• Derivative Risk Index

• Options Intention-to-Trade Ratio

• Derivatives Trading Volume

• Options Implied Volatility

• Profit and Loss Transfer Amount

• New and Active Addresses

• Net Longs on Clementine Exchange

• Net Longs on Elderberry Exchange

• High-Weighted Selling Pressure

• Global Buying Power Status

• Stablecoin Exchange Net Longs

• Off-chain Exchange Data

Derivatives Rating: The Risk Index is in the red zone, indicating an increase in derivative risk.

(See Derivative Risk Index below)

Last week, the market experienced a rapid decline, and with the rebound, the Risk Index has once again entered the red zone. As market sentiment has not fully recovered, it is expected that this week, derivatives will likely undergo a "long and short double burst."

(See Options Intention-to-Trade Ratio below)

The ratio and volume of put options have both declined, but the current put options ratio remains high.

(Derivative Trading Volume Chart)

Derivative trading volume has dropped to a relative low, but the derivative market is destined to not remain calm this week.

(Options Implied Volatility Chart)

Options implied volatility has experienced rapid fluctuations in the short term. Sentiment rating: Neutral

(Profit and Loss Transfer Amount Chart)

It was mentioned last week that if the orange line (panic selling) touches the phase peak again, it would be a relatively good buy-the-dip trading range. This week, both market panic and positive sentiment have once again receded, and the expected future rebound may be limited even in the short term.

(New and Active Addresses Chart)

New active addresses are at a medium to low level. Spot market and selling pressure structure rating: Both BTC and ETH have seen significant outflows.

(Citrus Swap Exchange Net Flow)

Currently, BTC has seen significant outflows.

(Ethereum Exchange Net Flow)

Currently, ETH has seen significant outflows.

(Heavy Selling Pressure)

Heavy selling pressure has eased.

Buying Power Rating: Global buying power is in a slight recovery state, stablecoin buying power is showing a minor rebound.

(Global Purchasing Power Status)

The global purchasing power has currently shifted from a declining trend to a very weak rebound.

(USDT Exchange Net Flow)

The stablecoin purchasing power has seen a slight recovery.

Off-chain transaction data rating: There is buying interest at 75000; there is selling interest at 90000.

(Coinbase Off-chain Data)

There is buying interest around 70000-75000;

There is selling interest at 90000.

(Binance Off-chain Data)

There is buying interest around 70000-75000;

There is selling interest at 90000.

(Bitfinex Off-chain Data)

There is buying interest around 76000;

Weekly Summary:

News Summary:

The current market situation is a mix of severe macroeconomic uncertainty and structural developments within the crypto asset space. The U.S. economy is facing recession concerns (yield curve inversion warning, rising joblessness expectations) and potential inflationary pressures (tariff impacts, previous inflation data), leading to highly uncertain Fed rate policy trajectory, becoming a core market focus. Significant volatility in the U.S. Treasury market (Dimon's warning, recent sell-offs) and the unpredictable tariff policy further exacerbate market confidence wobbles on the economic and policy front, boosting safe-haven assets (gold hitting record highs) and dampening risk appetite.

In this context, although the cryptocurrency market is under pressure, it has shown internal resilience: the U.S. regulatory environment is becoming clearer (infrastructure bill, stablecoin bill advancing), institutions continue to enter (BlackRock fund growth, MicroStrategy increasing holdings), simple metrics (on-chain data) suggest a potential bottom, and the stablecoin ecosystem remains active.

Looking ahead, the trajectory of cryptocurrency will heavily depend on macroeconomic developments: if an economic slowdown prompts the Fed to cut interest rates and inject liquidity, while regulation continues to advance, the crypto market is expected to benefit from a risk-on sentiment recovery and the potential "digital gold" narrative; conversely, if stubborn inflation or severe recession leads to persistent tightening or extreme risk aversion, the crypto market faces significant downside risk. Therefore, although the cryptocurrency industry's fundamentals are improving, its short-term performance is still expected to closely follow macroeconomic trends and Fed policy, with high market volatility expected to persist.

On-chain Long-term Insights:

1. The growth rate of illiquid supply has recently significantly slowed down, indicating that the marginal accumulation momentum of long-term whales is weakening at a high level;

2. Although the long-term holder base appears stable, the supply aging rate is slowing down, and short-term holders account for a higher proportion, signaling a market entering a period of structural adjustment;

3. Large fund flows on exchanges show a significant two-way tug-of-war, reflecting that large holders have clear disagreements and game theory at the current price level;

4. The outflow pressure of U.S. Bitcoin spot ETF funds has weakened, with recent periods even showing unstable inflows and outflows coexisting, indicating that selling pressure and demand coexist.

• Market Outlook:

Selling pressure and buying demand coexist.

The current market is at a critical stage of consolidation near highs, with bulls and bears fiercely battling around key price levels.

Therefore, in the short term, the market may continue its oscillating adjustment pattern, with the future direction highly dependent on the clarification of macroeconomic signals and the emergence of new demand catalysts.

On-chain Mid-term Exploration:

1. Whales have become an important market holding group.

2. Short-term profits are healthy, with emotions shifting.

3. Current price level has high holding value, and selling pressure is declining.

4. Currently above oversold levels (79000), buying power is waiting to increase.

5. Market sentiment is swinging, with liquidity direction unclear.

• Market Tone:

Lingering

The market has a large support group but is still hovering overall, with uncertain and swinging emotions. A relatively choppy assessment may align with the current tone.

On-Chain Short-Term Observations:

1. The risk factor is in the red zone, increasing the risk of derivatives.

2. New active addresses are relatively low.

3. Market sentiment rating: Neutral.

4. Net headroom on exchanges shows significant outflows of both BTC and ETH.

5. Global purchasing power is slightly rebounding, with stablecoin purchasing power showing a minor increase.

6. Off-chain transaction data indicates buying interest at 75000; selling interest at 90000.

7. In the short term, the probability of not dropping below 70000-75000 is 70%; with an 80% probability of not rising above 85000-90000 in the short term.

• Market Tone:

For BTC, the short-term market is quite "calm," even in the face of significant volatility, without triggering true panic selling.

Short-Term Outlook

This week, the derivative market may experience significant volatility, with prices potentially facing resistance at the short-term holder cost line (92k).

Risk Advisory:

The above is all market discussion and exploration, not investment advice; please be cautious and guard against market black swan risks.

This article is a submission and does not represent the views of BlockBeats.

You may also like

Token Cannot Compound, Where Is the Real Investment Opportunity?

February 6th Market Key Intelligence, How Much Did You Miss?

China's Central Bank and Eight Other Departments' Latest Regulatory Focus: Key Attention to RWA Tokenized Asset Risk

Foreword: Today, the People's Bank of China's website published the "Notice of the People's Bank of China, National Development and Reform Commission, Ministry of Industry and Information Technology, Ministry of Public Security, State Administration for Market Regulation, China Banking and Insurance Regulatory Commission, China Securities Regulatory Commission, State Administration of Foreign Exchange on Further Preventing and Dealing with Risks Related to Virtual Currency and Others (Yinfa [2026] No. 42)", the latest regulatory requirements from the eight departments including the central bank, which are basically consistent with the regulatory requirements of recent years. The main focus of the regulation is on speculative activities such as virtual currency trading, exchanges, ICOs, overseas platform services, and this time, regulatory oversight of RWA has been added, explicitly prohibiting RWA tokenization, stablecoins (especially those pegged to the RMB). The following is the full text:

To the people's governments of all provinces, autonomous regions, and municipalities directly under the Central Government, the Xinjiang Production and Construction Corps:

Recently, there have been speculative activities related to virtual currency and Real-World Assets (RWA) tokenization, disrupting the economic and financial order and jeopardizing the property security of the people. In order to further prevent and address the risks related to virtual currency and Real-World Assets tokenization, effectively safeguard national security and social stability, in accordance with the "Law of the People's Republic of China on the People's Bank of China," "Law of the People's Republic of China on Commercial Banks," "Securities Law of the People's Republic of China," "Law of the People's Republic of China on Securities Investment Funds," "Law of the People's Republic of China on Futures and Derivatives," "Cybersecurity Law of the People's Republic of China," "Regulations of the People's Republic of China on the Administration of Renminbi," "Regulations on Prevention and Disposal of Illegal Fundraising," "Regulations of the People's Republic of China on Foreign Exchange Administration," "Telecommunications Regulations of the People's Republic of China," and other provisions, after reaching consensus with the Cyberspace Administration of China, the Supreme People's Court, and the Supreme People's Procuratorate, and with the approval of the State Council, the relevant matters are notified as follows:

(I) Virtual currency does not possess the legal status equivalent to fiat currency. Virtual currencies such as Bitcoin, Ether, Tether, etc., have the main characteristics of being issued by non-monetary authorities, using encryption technology and distributed ledger or similar technology, existing in digital form, etc. They do not have legal tender status, should not and cannot be circulated and used as currency in the market.

The business activities related to virtual currency are classified as illegal financial activities. The exchange of fiat currency and virtual currency within the territory, exchange of virtual currencies, acting as a central counterparty in buying and selling virtual currencies, providing information intermediary and pricing services for virtual currency transactions, token issuance financing, and trading of virtual currency-related financial products, etc., fall under illegal financial activities, such as suspected illegal issuance of token vouchers, unauthorized public issuance of securities, illegal operation of securities and futures business, illegal fundraising, etc., are strictly prohibited across the board and resolutely banned in accordance with the law. Overseas entities and individuals are not allowed to provide virtual currency-related services to domestic entities in any form.

A stablecoin pegged to a fiat currency indirectly fulfills some functions of the fiat currency in circulation. Without the consent of relevant authorities in accordance with the law and regulations, any domestic or foreign entity or individual is not allowed to issue a RMB-pegged stablecoin overseas.

(II)Tokenization of Real-World Assets refers to the use of encryption technology and distributed ledger or similar technologies to transform ownership rights, income rights, etc., of assets into tokens (tokens) or other interests or bond certificates with token (token) characteristics, and carry out issuance and trading activities.

Engaging in the tokenization of real-world assets domestically, as well as providing related intermediary, information technology services, etc., which are suspected of illegal issuance of token vouchers, unauthorized public offering of securities, illegal operation of securities and futures business, illegal fundraising, and other illegal financial activities, shall be prohibited; except for relevant business activities carried out with the approval of the competent authorities in accordance with the law and regulations and relying on specific financial infrastructures. Overseas entities and individuals are not allowed to illegally provide services related to the tokenization of real-world assets to domestic entities in any form.

(III) Inter-agency Coordination. The People's Bank of China, together with the National Development and Reform Commission, the Ministry of Industry and Information Technology, the Ministry of Public Security, the State Administration for Market Regulation, the China Banking and Insurance Regulatory Commission, the China Securities Regulatory Commission, the State Administration of Foreign Exchange, and other departments, will improve the work mechanism, strengthen coordination with the Cyberspace Administration of China, the Supreme People's Court, and the Supreme People's Procuratorate, coordinate efforts, and overall guide regions to carry out risk prevention and disposal of virtual currency-related illegal financial activities.

The China Securities Regulatory Commission, together with the National Development and Reform Commission, the Ministry of Industry and Information Technology, the Ministry of Public Security, the People's Bank of China, the State Administration for Market Regulation, the China Banking and Insurance Regulatory Commission, the State Administration of Foreign Exchange, and other departments, will improve the work mechanism, strengthen coordination with the Cyberspace Administration of China, the Supreme People's Court, and the Supreme People's Procuratorate, coordinate efforts, and overall guide regions to carry out risk prevention and disposal of illegal financial activities related to the tokenization of real-world assets.

(IV) Strengthening Local Implementation. The people's governments at the provincial level are overall responsible for the prevention and disposal of risks related to virtual currencies and the tokenization of real-world assets in their respective administrative regions. The specific leading department is the local financial regulatory department, with participation from branches and dispatched institutions of the State Council's financial regulatory department, telecommunications regulators, public security, market supervision, and other departments, in coordination with cyberspace departments, courts, and procuratorates, to improve the normalization of the work mechanism, effectively connect with the relevant work mechanisms of central departments, form a cooperative and coordinated working pattern between central and local governments, effectively prevent and properly handle risks related to virtual currencies and the tokenization of real-world assets, and maintain economic and financial order and social stability.

(5) Enhanced Risk Monitoring. The People's Bank of China, China Securities Regulatory Commission, National Development and Reform Commission, Ministry of Industry and Information Technology, Ministry of Public Security, State Administration of Foreign Exchange, Cyberspace Administration of China, and other departments continue to improve monitoring techniques and system support, enhance cross-departmental data analysis and sharing, establish sound information sharing and cross-validation mechanisms, promptly grasp the risk situation of activities related to virtual currency and real-world asset tokenization. Local governments at all levels give full play to the role of local monitoring and early warning mechanisms. Local financial regulatory authorities, together with branches and agencies of the State Council's financial regulatory authorities, as well as departments of cyberspace and public security, ensure effective connection between online monitoring, offline investigation, and fund tracking, efficiently and accurately identify activities related to virtual currency and real-world asset tokenization, promptly share risk information, improve early warning information dissemination, verification, and rapid response mechanisms.

(6) Strengthened Oversight of Financial Institutions, Intermediaries, and Technology Service Providers. Financial institutions (including non-bank payment institutions) are prohibited from providing account opening, fund transfer, and clearing services for virtual currency-related business activities, issuing and selling financial products related to virtual currency, including virtual currency and related financial products in the scope of collateral, conducting insurance business related to virtual currency, or including virtual currency in the scope of insurance liability. Financial institutions (including non-bank payment institutions) are prohibited from providing custody, clearing, and settlement services for unauthorized real-world asset tokenization-related business and related financial products. Relevant intermediary institutions and information technology service providers are prohibited from providing intermediary, technical, or other services for unauthorized real-world asset tokenization-related businesses and related financial products.

(7) Enhanced Management of Internet Information Content and Access. Internet enterprises are prohibited from providing online business venues, commercial displays, marketing, advertising, or paid traffic diversion services for virtual currency and real-world asset tokenization-related business activities. Upon discovering clues of illegal activities, they should promptly report to relevant departments and provide technical support and assistance for related investigations and inquiries. Based on the clues transferred by the financial regulatory authorities, the cyberspace administration, telecommunications authorities, and public security departments should promptly close and deal with websites, mobile applications (including mini-programs), and public accounts engaged in virtual currency and real-world asset tokenization-related business activities in accordance with the law.

(8) Strengthened Entity Registration and Advertisement Management. Market supervision departments strengthen entity registration and management, and enterprise and individual business registrations must not contain terms such as "virtual currency," "virtual asset," "cryptocurrency," "crypto asset," "stablecoin," "real-world asset tokenization," or "RWA" in their names or business scopes. Market supervision departments, together with financial regulatory authorities, legally enhance the supervision of advertisements related to virtual currency and real-world asset tokenization, promptly investigating and handling relevant illegal advertisements.

(IX) Continued Rectification of Virtual Currency Mining Activities. The National Development and Reform Commission, together with relevant departments, strictly controls virtual currency mining activities, continuously promotes the rectification of virtual currency mining activities. The people's governments of various provinces take overall responsibility for the rectification of "mining" within their respective administrative regions. In accordance with the requirements of the National Development and Reform Commission and other departments in the "Notice on the Rectification of Virtual Currency Mining Activities" (NDRC Energy-saving Building [2021] No. 1283) and the provisions of the "Guidance Catalog for Industrial Structure Adjustment (2024 Edition)," a comprehensive review, investigation, and closure of existing virtual currency mining projects are conducted, new mining projects are strictly prohibited, and mining machine production enterprises are strictly prohibited from providing mining machine sales and other services within the country.

(X) Severe Crackdown on Related Illegal Financial Activities. Upon discovering clues to illegal financial activities related to virtual currency and the tokenization of real-world assets, local financial regulatory authorities, branches of the State Council's financial regulatory authorities, and other relevant departments promptly investigate, determine, and properly handle the issues in accordance with the law, and seriously hold the relevant entities and individuals legally responsible. Those suspected of crimes are transferred to the judicial authorities for processing according to the law.

(XI) Severe Crackdown on Related Illegal and Criminal Activities. The Ministry of Public Security, the People's Bank of China, the State Administration for Market Regulation, the China Banking and Insurance Regulatory Commission, the China Securities Regulatory Commission, as well as judicial and procuratorial organs, in accordance with their respective responsibilities, rigorously crack down on illegal and criminal activities related to virtual currency, the tokenization of real-world assets, such as fraud, money laundering, illegal business operations, pyramid schemes, illegal fundraising, and other illegal and criminal activities carried out under the guise of virtual currency, the tokenization of real-world assets, etc.

(XII) Strengthen Industry Self-discipline. Relevant industry associations should enhance membership management and policy advocacy, based on their own responsibilities, advocate and urge member units to resist illegal financial activities related to virtual currency and the tokenization of real-world assets. Member units that violate regulatory policies and industry self-discipline rules are to be disciplined in accordance with relevant self-regulatory management regulations. By leveraging various industry infrastructure, conduct risk monitoring related to virtual currency, the tokenization of real-world assets, and promptly transfer issue clues to relevant departments.

(XIII) Without the approval of relevant departments in accordance with the law and regulations, domestic entities and foreign entities controlled by them may not issue virtual currency overseas.

(XIV) Domestic entities engaging directly or indirectly in overseas external debt-based tokenization of real-world assets, or conducting asset securitization activities abroad based on domestic ownership rights, income rights, etc. (hereinafter referred to as domestic equity), should be strictly regulated in accordance with the principles of "same business, same risk, same rules." The National Development and Reform Commission, the China Securities Regulatory Commission, the State Administration of Foreign Exchange, and other relevant departments regulate it according to their respective responsibilities. For other forms of overseas real-world asset tokenization activities based on domestic equity by domestic entities, the China Securities Regulatory Commission, together with relevant departments, supervise according to their division of responsibilities. Without the consent and filing of relevant departments, no unit or individual may engage in the above-mentioned business.

(15) Overseas subsidiaries and branches of domestic financial institutions providing Real World Asset Tokenization-related services overseas shall do so legally and prudently. They shall have professional personnel and systems in place to effectively mitigate business risks, strictly implement customer onboarding, suitability management, anti-money laundering requirements, and incorporate them into the domestic financial institutions' compliance and risk management system. Intermediaries and information technology service providers offering Real World Asset Tokenization services abroad based on domestic equity or conducting Real World Asset Tokenization business in the form of overseas debt for domestic entities directly or indirectly venturing abroad must strictly comply with relevant laws and regulations. They should establish and improve relevant compliance and internal control systems in accordance with relevant normative requirements, strengthen business and risk control, and report the business developments to the relevant regulatory authorities for approval or filing.

(16) Strengthen organizational leadership and overall coordination. All departments and regions should attach great importance to the prevention of risks related to virtual currencies and Real World Asset Tokenization, strengthen organizational leadership, clarify work responsibilities, form a long-term effective working mechanism with centralized coordination, local implementation, and shared responsibilities, maintain high pressure, dynamically monitor risks, effectively prevent and mitigate risks in an orderly and efficient manner, legally protect the property security of the people, and make every effort to maintain economic and financial order and social stability.

(17) Widely carry out publicity and education. All departments, regions, and industry associations should make full use of various media and other communication channels to disseminate information through legal and policy interpretation, analysis of typical cases, and education on investment risks, etc. They should promote the illegality and harm of virtual currencies and Real World Asset Tokenization-related businesses and their manifestations, fully alert to potential risks and hidden dangers, and enhance public awareness and identification capabilities for risk prevention.

(18) Engaging in illegal financial activities related to virtual currencies and Real World Asset Tokenization in violation of this notice, as well as providing services for virtual currencies and Real World Asset Tokenization-related businesses, shall be punished in accordance with relevant regulations. If it constitutes a crime, criminal liability shall be pursued according to the law. For domestic entities and individuals who knowingly or should have known that overseas entities illegally provided virtual currency or Real World Asset Tokenization-related services to domestic entities and still assisted them, relevant responsibilities shall be pursued according to the law. If it constitutes a crime, criminal liability shall be pursued according to the law.

(19) If any unit or individual invests in virtual currencies, Real World Asset Tokens, and related financial products against public order and good customs, the relevant civil legal actions shall be invalid, and any resulting losses shall be borne by them. If there are suspicions of disrupting financial order and jeopardizing financial security, the relevant departments shall deal with them according to the law.

This notice shall enter into force upon the date of its issuance. The People's Bank of China and ten other departments' "Notice on Further Preventing and Dealing with the Risks of Virtual Currency Trading Speculation" (Yinfa [2021] No. 237) is hereby repealed.

Former Partner's Perspective on Multicoin: Kyle's Exit, But the Game He Left Behind Just Getting Started

Why Bitcoin Is Falling Now: The Real Reasons Behind BTC's Crash & WEEX's Smart Profit Playbook

Bitcoin's ongoing crash explained: Discover the 5 hidden triggers behind BTC's plunge & how WEEX's Auto Earn and Trade to Earn strategies help traders profit from crypto market volatility.

Wall Street's Hottest Trades See Exodus

Vitalik Discusses Ethereum Scaling Path, Circle Announces Partnership with Polymarket, What's the Overseas Crypto Community Talking About Today?

Believing in the Capital Markets - The Essence and Core Value of Cryptocurrency

Polymarket's 'Weatherman': Predict Temperature, Win Million-Dollar Payout

$15K+ Profits: The 4 AI Trading Secrets WEEX Hackathon Prelim Winners Used to Dominate Volatile Crypto Markets

How WEEX Hackathon's top AI trading strategies made $15K+ in crypto markets: 4 proven rules for ETH/BTC trading, market structure analysis, and risk management in volatile conditions.

A nearly 20% one-day plunge, how long has it been since you last saw a $60,000 Bitcoin?

Raoul Pal: I've seen every single panic, and they are never the end.

Key Market Information Discrepancy on February 6th - A Must-Read! | Alpha Morning Report

2026 Crypto Industry's First Snowfall

The Harsh Reality Behind the $26 Billion Crypto Liquidation: Liquidity Is Killing the Market

Why Is Gold, US Stocks, Bitcoin All Falling?

Key Market Intelligence for February 5th, how much did you miss out on?

Wintermute: By 2026, crypto had gradually become the settlement layer of the Internet economy

Token Cannot Compound, Where Is the Real Investment Opportunity?

February 6th Market Key Intelligence, How Much Did You Miss?

China's Central Bank and Eight Other Departments' Latest Regulatory Focus: Key Attention to RWA Tokenized Asset Risk

Foreword: Today, the People's Bank of China's website published the "Notice of the People's Bank of China, National Development and Reform Commission, Ministry of Industry and Information Technology, Ministry of Public Security, State Administration for Market Regulation, China Banking and Insurance Regulatory Commission, China Securities Regulatory Commission, State Administration of Foreign Exchange on Further Preventing and Dealing with Risks Related to Virtual Currency and Others (Yinfa [2026] No. 42)", the latest regulatory requirements from the eight departments including the central bank, which are basically consistent with the regulatory requirements of recent years. The main focus of the regulation is on speculative activities such as virtual currency trading, exchanges, ICOs, overseas platform services, and this time, regulatory oversight of RWA has been added, explicitly prohibiting RWA tokenization, stablecoins (especially those pegged to the RMB). The following is the full text:

To the people's governments of all provinces, autonomous regions, and municipalities directly under the Central Government, the Xinjiang Production and Construction Corps:

Recently, there have been speculative activities related to virtual currency and Real-World Assets (RWA) tokenization, disrupting the economic and financial order and jeopardizing the property security of the people. In order to further prevent and address the risks related to virtual currency and Real-World Assets tokenization, effectively safeguard national security and social stability, in accordance with the "Law of the People's Republic of China on the People's Bank of China," "Law of the People's Republic of China on Commercial Banks," "Securities Law of the People's Republic of China," "Law of the People's Republic of China on Securities Investment Funds," "Law of the People's Republic of China on Futures and Derivatives," "Cybersecurity Law of the People's Republic of China," "Regulations of the People's Republic of China on the Administration of Renminbi," "Regulations on Prevention and Disposal of Illegal Fundraising," "Regulations of the People's Republic of China on Foreign Exchange Administration," "Telecommunications Regulations of the People's Republic of China," and other provisions, after reaching consensus with the Cyberspace Administration of China, the Supreme People's Court, and the Supreme People's Procuratorate, and with the approval of the State Council, the relevant matters are notified as follows:

(I) Virtual currency does not possess the legal status equivalent to fiat currency. Virtual currencies such as Bitcoin, Ether, Tether, etc., have the main characteristics of being issued by non-monetary authorities, using encryption technology and distributed ledger or similar technology, existing in digital form, etc. They do not have legal tender status, should not and cannot be circulated and used as currency in the market.

The business activities related to virtual currency are classified as illegal financial activities. The exchange of fiat currency and virtual currency within the territory, exchange of virtual currencies, acting as a central counterparty in buying and selling virtual currencies, providing information intermediary and pricing services for virtual currency transactions, token issuance financing, and trading of virtual currency-related financial products, etc., fall under illegal financial activities, such as suspected illegal issuance of token vouchers, unauthorized public issuance of securities, illegal operation of securities and futures business, illegal fundraising, etc., are strictly prohibited across the board and resolutely banned in accordance with the law. Overseas entities and individuals are not allowed to provide virtual currency-related services to domestic entities in any form.

A stablecoin pegged to a fiat currency indirectly fulfills some functions of the fiat currency in circulation. Without the consent of relevant authorities in accordance with the law and regulations, any domestic or foreign entity or individual is not allowed to issue a RMB-pegged stablecoin overseas.

(II)Tokenization of Real-World Assets refers to the use of encryption technology and distributed ledger or similar technologies to transform ownership rights, income rights, etc., of assets into tokens (tokens) or other interests or bond certificates with token (token) characteristics, and carry out issuance and trading activities.

Engaging in the tokenization of real-world assets domestically, as well as providing related intermediary, information technology services, etc., which are suspected of illegal issuance of token vouchers, unauthorized public offering of securities, illegal operation of securities and futures business, illegal fundraising, and other illegal financial activities, shall be prohibited; except for relevant business activities carried out with the approval of the competent authorities in accordance with the law and regulations and relying on specific financial infrastructures. Overseas entities and individuals are not allowed to illegally provide services related to the tokenization of real-world assets to domestic entities in any form.

(III) Inter-agency Coordination. The People's Bank of China, together with the National Development and Reform Commission, the Ministry of Industry and Information Technology, the Ministry of Public Security, the State Administration for Market Regulation, the China Banking and Insurance Regulatory Commission, the China Securities Regulatory Commission, the State Administration of Foreign Exchange, and other departments, will improve the work mechanism, strengthen coordination with the Cyberspace Administration of China, the Supreme People's Court, and the Supreme People's Procuratorate, coordinate efforts, and overall guide regions to carry out risk prevention and disposal of virtual currency-related illegal financial activities.

The China Securities Regulatory Commission, together with the National Development and Reform Commission, the Ministry of Industry and Information Technology, the Ministry of Public Security, the People's Bank of China, the State Administration for Market Regulation, the China Banking and Insurance Regulatory Commission, the State Administration of Foreign Exchange, and other departments, will improve the work mechanism, strengthen coordination with the Cyberspace Administration of China, the Supreme People's Court, and the Supreme People's Procuratorate, coordinate efforts, and overall guide regions to carry out risk prevention and disposal of illegal financial activities related to the tokenization of real-world assets.

(IV) Strengthening Local Implementation. The people's governments at the provincial level are overall responsible for the prevention and disposal of risks related to virtual currencies and the tokenization of real-world assets in their respective administrative regions. The specific leading department is the local financial regulatory department, with participation from branches and dispatched institutions of the State Council's financial regulatory department, telecommunications regulators, public security, market supervision, and other departments, in coordination with cyberspace departments, courts, and procuratorates, to improve the normalization of the work mechanism, effectively connect with the relevant work mechanisms of central departments, form a cooperative and coordinated working pattern between central and local governments, effectively prevent and properly handle risks related to virtual currencies and the tokenization of real-world assets, and maintain economic and financial order and social stability.

(5) Enhanced Risk Monitoring. The People's Bank of China, China Securities Regulatory Commission, National Development and Reform Commission, Ministry of Industry and Information Technology, Ministry of Public Security, State Administration of Foreign Exchange, Cyberspace Administration of China, and other departments continue to improve monitoring techniques and system support, enhance cross-departmental data analysis and sharing, establish sound information sharing and cross-validation mechanisms, promptly grasp the risk situation of activities related to virtual currency and real-world asset tokenization. Local governments at all levels give full play to the role of local monitoring and early warning mechanisms. Local financial regulatory authorities, together with branches and agencies of the State Council's financial regulatory authorities, as well as departments of cyberspace and public security, ensure effective connection between online monitoring, offline investigation, and fund tracking, efficiently and accurately identify activities related to virtual currency and real-world asset tokenization, promptly share risk information, improve early warning information dissemination, verification, and rapid response mechanisms.

(6) Strengthened Oversight of Financial Institutions, Intermediaries, and Technology Service Providers. Financial institutions (including non-bank payment institutions) are prohibited from providing account opening, fund transfer, and clearing services for virtual currency-related business activities, issuing and selling financial products related to virtual currency, including virtual currency and related financial products in the scope of collateral, conducting insurance business related to virtual currency, or including virtual currency in the scope of insurance liability. Financial institutions (including non-bank payment institutions) are prohibited from providing custody, clearing, and settlement services for unauthorized real-world asset tokenization-related business and related financial products. Relevant intermediary institutions and information technology service providers are prohibited from providing intermediary, technical, or other services for unauthorized real-world asset tokenization-related businesses and related financial products.

(7) Enhanced Management of Internet Information Content and Access. Internet enterprises are prohibited from providing online business venues, commercial displays, marketing, advertising, or paid traffic diversion services for virtual currency and real-world asset tokenization-related business activities. Upon discovering clues of illegal activities, they should promptly report to relevant departments and provide technical support and assistance for related investigations and inquiries. Based on the clues transferred by the financial regulatory authorities, the cyberspace administration, telecommunications authorities, and public security departments should promptly close and deal with websites, mobile applications (including mini-programs), and public accounts engaged in virtual currency and real-world asset tokenization-related business activities in accordance with the law.

(8) Strengthened Entity Registration and Advertisement Management. Market supervision departments strengthen entity registration and management, and enterprise and individual business registrations must not contain terms such as "virtual currency," "virtual asset," "cryptocurrency," "crypto asset," "stablecoin," "real-world asset tokenization," or "RWA" in their names or business scopes. Market supervision departments, together with financial regulatory authorities, legally enhance the supervision of advertisements related to virtual currency and real-world asset tokenization, promptly investigating and handling relevant illegal advertisements.

(IX) Continued Rectification of Virtual Currency Mining Activities. The National Development and Reform Commission, together with relevant departments, strictly controls virtual currency mining activities, continuously promotes the rectification of virtual currency mining activities. The people's governments of various provinces take overall responsibility for the rectification of "mining" within their respective administrative regions. In accordance with the requirements of the National Development and Reform Commission and other departments in the "Notice on the Rectification of Virtual Currency Mining Activities" (NDRC Energy-saving Building [2021] No. 1283) and the provisions of the "Guidance Catalog for Industrial Structure Adjustment (2024 Edition)," a comprehensive review, investigation, and closure of existing virtual currency mining projects are conducted, new mining projects are strictly prohibited, and mining machine production enterprises are strictly prohibited from providing mining machine sales and other services within the country.

(X) Severe Crackdown on Related Illegal Financial Activities. Upon discovering clues to illegal financial activities related to virtual currency and the tokenization of real-world assets, local financial regulatory authorities, branches of the State Council's financial regulatory authorities, and other relevant departments promptly investigate, determine, and properly handle the issues in accordance with the law, and seriously hold the relevant entities and individuals legally responsible. Those suspected of crimes are transferred to the judicial authorities for processing according to the law.

(XI) Severe Crackdown on Related Illegal and Criminal Activities. The Ministry of Public Security, the People's Bank of China, the State Administration for Market Regulation, the China Banking and Insurance Regulatory Commission, the China Securities Regulatory Commission, as well as judicial and procuratorial organs, in accordance with their respective responsibilities, rigorously crack down on illegal and criminal activities related to virtual currency, the tokenization of real-world assets, such as fraud, money laundering, illegal business operations, pyramid schemes, illegal fundraising, and other illegal and criminal activities carried out under the guise of virtual currency, the tokenization of real-world assets, etc.

(XII) Strengthen Industry Self-discipline. Relevant industry associations should enhance membership management and policy advocacy, based on their own responsibilities, advocate and urge member units to resist illegal financial activities related to virtual currency and the tokenization of real-world assets. Member units that violate regulatory policies and industry self-discipline rules are to be disciplined in accordance with relevant self-regulatory management regulations. By leveraging various industry infrastructure, conduct risk monitoring related to virtual currency, the tokenization of real-world assets, and promptly transfer issue clues to relevant departments.

(XIII) Without the approval of relevant departments in accordance with the law and regulations, domestic entities and foreign entities controlled by them may not issue virtual currency overseas.

(XIV) Domestic entities engaging directly or indirectly in overseas external debt-based tokenization of real-world assets, or conducting asset securitization activities abroad based on domestic ownership rights, income rights, etc. (hereinafter referred to as domestic equity), should be strictly regulated in accordance with the principles of "same business, same risk, same rules." The National Development and Reform Commission, the China Securities Regulatory Commission, the State Administration of Foreign Exchange, and other relevant departments regulate it according to their respective responsibilities. For other forms of overseas real-world asset tokenization activities based on domestic equity by domestic entities, the China Securities Regulatory Commission, together with relevant departments, supervise according to their division of responsibilities. Without the consent and filing of relevant departments, no unit or individual may engage in the above-mentioned business.

(15) Overseas subsidiaries and branches of domestic financial institutions providing Real World Asset Tokenization-related services overseas shall do so legally and prudently. They shall have professional personnel and systems in place to effectively mitigate business risks, strictly implement customer onboarding, suitability management, anti-money laundering requirements, and incorporate them into the domestic financial institutions' compliance and risk management system. Intermediaries and information technology service providers offering Real World Asset Tokenization services abroad based on domestic equity or conducting Real World Asset Tokenization business in the form of overseas debt for domestic entities directly or indirectly venturing abroad must strictly comply with relevant laws and regulations. They should establish and improve relevant compliance and internal control systems in accordance with relevant normative requirements, strengthen business and risk control, and report the business developments to the relevant regulatory authorities for approval or filing.

(16) Strengthen organizational leadership and overall coordination. All departments and regions should attach great importance to the prevention of risks related to virtual currencies and Real World Asset Tokenization, strengthen organizational leadership, clarify work responsibilities, form a long-term effective working mechanism with centralized coordination, local implementation, and shared responsibilities, maintain high pressure, dynamically monitor risks, effectively prevent and mitigate risks in an orderly and efficient manner, legally protect the property security of the people, and make every effort to maintain economic and financial order and social stability.

(17) Widely carry out publicity and education. All departments, regions, and industry associations should make full use of various media and other communication channels to disseminate information through legal and policy interpretation, analysis of typical cases, and education on investment risks, etc. They should promote the illegality and harm of virtual currencies and Real World Asset Tokenization-related businesses and their manifestations, fully alert to potential risks and hidden dangers, and enhance public awareness and identification capabilities for risk prevention.

(18) Engaging in illegal financial activities related to virtual currencies and Real World Asset Tokenization in violation of this notice, as well as providing services for virtual currencies and Real World Asset Tokenization-related businesses, shall be punished in accordance with relevant regulations. If it constitutes a crime, criminal liability shall be pursued according to the law. For domestic entities and individuals who knowingly or should have known that overseas entities illegally provided virtual currency or Real World Asset Tokenization-related services to domestic entities and still assisted them, relevant responsibilities shall be pursued according to the law. If it constitutes a crime, criminal liability shall be pursued according to the law.

(19) If any unit or individual invests in virtual currencies, Real World Asset Tokens, and related financial products against public order and good customs, the relevant civil legal actions shall be invalid, and any resulting losses shall be borne by them. If there are suspicions of disrupting financial order and jeopardizing financial security, the relevant departments shall deal with them according to the law.

This notice shall enter into force upon the date of its issuance. The People's Bank of China and ten other departments' "Notice on Further Preventing and Dealing with the Risks of Virtual Currency Trading Speculation" (Yinfa [2021] No. 237) is hereby repealed.

Former Partner's Perspective on Multicoin: Kyle's Exit, But the Game He Left Behind Just Getting Started

Why Bitcoin Is Falling Now: The Real Reasons Behind BTC's Crash & WEEX's Smart Profit Playbook

Bitcoin's ongoing crash explained: Discover the 5 hidden triggers behind BTC's plunge & how WEEX's Auto Earn and Trade to Earn strategies help traders profit from crypto market volatility.