China's AI Compute Power Counterstrike

Article | Sleepy.txt

Eight years ago, ZTE suffered a sudden cardiac arrest.

On April 16, 2018, a ban from the U.S. Department of Commerce's Bureau of Industry and Security brought ZTE, the world's fourth-largest telecommunications equipment provider with 80,000 employees and annual revenue exceeding a hundred billion, to a standstill overnight. The ban was simple: for the next seven years, it prohibited any U.S. company from selling parts, goods, software, or technology to ZTE.

Without Qualcomm's chips, base stations ceased production. Without Google's Android license, phones were left without a usable system. Twenty-three days later, ZTE announced that its main business operations had become impossible.

However, ZTE ultimately survived, but at a cost of 1.4 billion U.S. dollars.

A $1 billion fine, to be paid in a lump sum; a $400 million escrow deposit, placed in a U.S. bank's custody account. In addition, a complete overhaul of all executives, accepting the presence of a U.S. compliance oversight team. In 2018, ZTE incurred a net loss of 7 billion RMB for the full year, with a year-on-year revenue plummet of 21.4%.

In an internal memo, then ZTE Chairman Yin Yimin wrote, "We are in a complex industry that heavily relies on the global supply chain." At that time, this statement was both reflective and resigned.

Eight years later, on February 26, 2026, Chinese AI unicorn DeepSeek announced that its upcoming V4 multimodal large model would prioritize deep collaboration with domestic chip manufacturers, achieving for the first time a full-process non-NVIDIA solution from pre-training to fine-tuning.

To put it simply: we no longer need NVIDIA.

Upon hearing this news, the market's initial reaction was skepticism. With NVIDIA holding over 90% of the global AI training chip market share, is it commercially reasonable to abandon it?

However, behind DeepSeek's choice lies a question much larger than business logic: What kind of computing independence does Chinese AI truly need?

What Was Really Choking Us

Many people think that the chip ban was blocking hardware. But what truly suffocated Chinese AI companies was something called CUDA.

CUDA, short for Compute Unified Device Architecture, is a parallel computing platform and programming model introduced by NVIDIA in 2006. It allows developers to directly harness the computing power of NVIDIA GPUs to accelerate various complex computing tasks.

Before the AI era, this was just a tool for a small number of geeks. But when the wave of deep learning arrived, CUDA became the foundation of the entire AI industry.

The training of AI large models is essentially massive matrix operations, which happens to be GPU's strong suit.

Thanks to NVIDIA's early positioning, CUDA has provided a complete toolchain from low-level hardware to upper-level applications for AI developers worldwide. Today, all mainstream AI frameworks globally, from Google's TensorFlow to Meta's PyTorch, are deeply integrated with CUDA at the core.

An AI Ph.D. student, from day one of enrollment, learns, programs, and experiments in the CUDA environment. Every line of code they write reinforces NVIDIA's moat.

By 2025, the CUDA ecosystem has attracted over 4.5 million developers, covering 3000+ GPU-accelerated applications, with over 40,000 companies worldwide using CUDA. This number means that over 90% of AI developers globally are locked into NVIDIA's ecosystem.

The frightening aspect of CUDA is that it is a flywheel. The more developers use it, the more tools, libraries, and code are generated, making the ecosystem more prosperous. The more prosperous the ecosystem, the more developers it attracts. Once this flywheel starts spinning, it is almost impossible to shake.

The result is that NVIDIA sells you the most expensive shovel and defines the only mining posture. Want to switch shovels? You can. But first, you have to rewrite all the experience, tools, and code accumulated by hundreds of thousands of the world's smartest brains over the past decade in this posture.

Who bears this cost?

So when on October 7, 2022, the first round of BIS regulations landed, restricting the export of NVIDIA A100 and H100 to China, Chinese AI companies collectively experienced a ZTE-style suffocation for the first time. NVIDIA subsequently launched the "China Special Edition" A800 and H800, reducing the interchip bandwidth to barely maintain supply.

However, just one year later, on October 17, 2023, the second round of regulations tightened again, and A800 and H800 were also banned, with 13 Chinese companies being added to the entity list. NVIDIA had to introduce the further castrated H20. By December 2024, in the final round of regulations during the Biden administration's term, even the export of H20 was severely restricted.

Tripartite Control, Layered Escalation.

But this time, the storyline is completely different from ZTE's back then.

An Asymmetric Breakout

Under the ban, everyone thought that China's AI dream of large models would come to an end.

They were all wrong. Faced with the blockade, Chinese companies did not choose a head-on confrontation but instead embarked on a breakout. The first battlefield of this breakout was not in chips but in algorithms.

From late 2024 to 2025, Chinese AI companies collectively shifted to a technical direction: Hybrid Expert Models.

In simple terms, it is splitting a huge model into many small experts, activating only the most relevant ones during tasks, rather than having the entire model in motion.

DeepSeek's V3 is a typical representative of this approach. It has 671 billion parameters, but only activates 37 billion of them during each inference, accounting for just 5.5% of the total. In terms of training costs, it used 2048 NVIDIA H800 GPUs, took 58 days to train, and cost a total of 5.576 million dollars. For comparison, the estimated training cost of GPT-4 is around 78 million dollars. A difference of an order of magnitude.

The extreme optimization on algorithms is directly reflected in the pricing. DeepSeek's API price is only $0.028 to $0.28 per million tokens for input and $0.42 per output, while GPT-4's input price is $5, and output is $15. Claude Opus is even more expensive, with input at $15 and output at $75. By conversion, DeepSeek is 25 to 75 times cheaper than Claude.

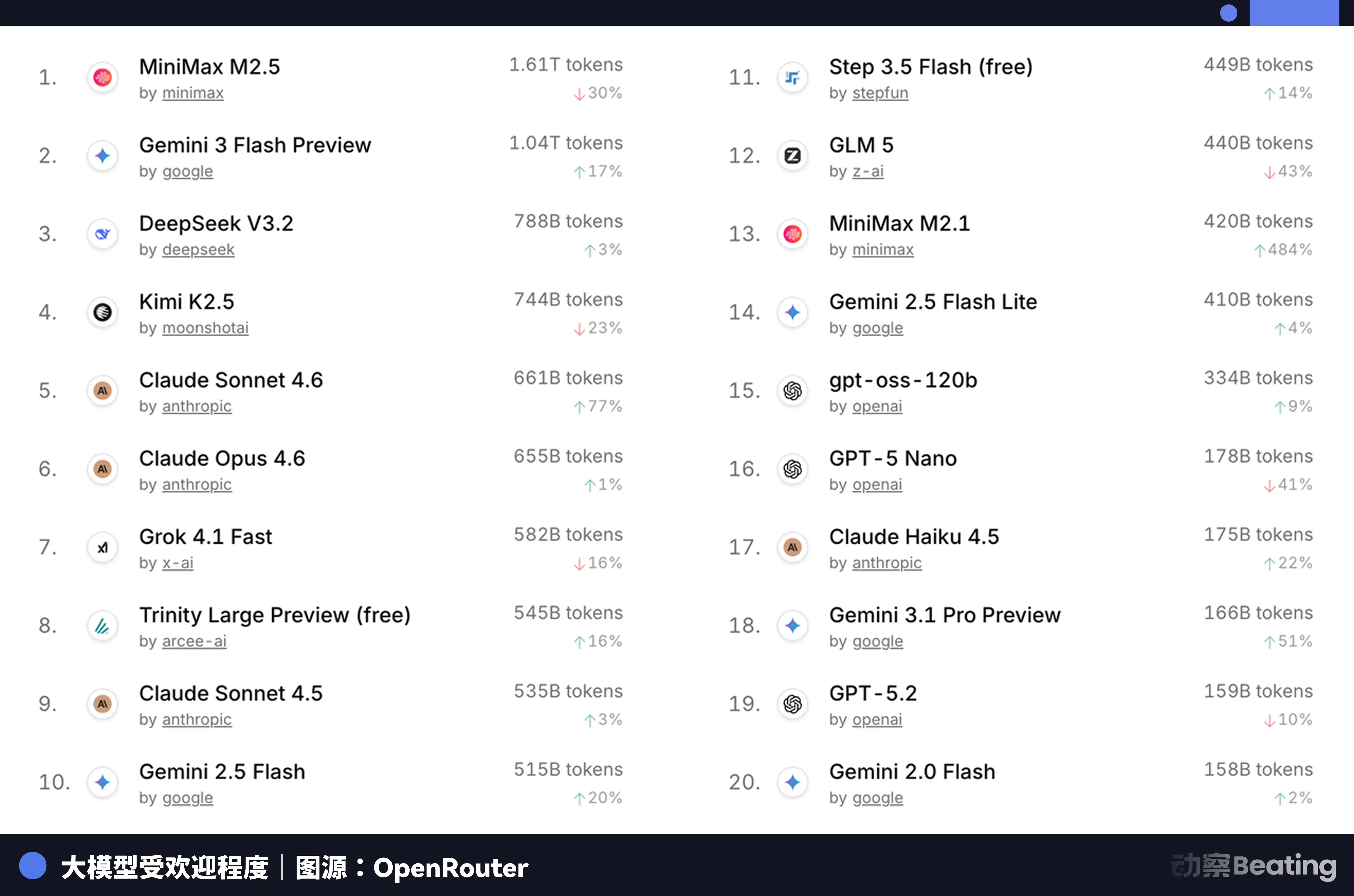

This price difference had a significant impact on the global developer market. In February 2026, on OpenRouter, the world's largest AI model API aggregation platform, China's AI model weekly call volume surged by 127% within three weeks, surpassing the United States for the first time. A year ago, China's model share on OpenRouter was less than 2%. A year later, it had grown by 421%, approaching sixty percent.

Behind this data is a structurally overlooked change. Starting in the second half of 2025, the mainstream scenario for AI applications shifted from chat to Agent. In an Agent scenario, the token consumption per task is 10 to 100 times that of simple chat. When token consumption grows exponentially, price becomes a decisive factor. The extreme cost-effectiveness of Chinese models happened to hit this window.

However, the problem is that the reduction in inference costs has not solved the fundamental issue of training. If a large model cannot sustain training and iteration on the latest data, its capability quickly degrades. And training remains the unavoidable power-hungry black hole.

So, where does the "shovel" for training come from?

The Promotion of Reserves

Xinghua, Jiangsu, a small city in central Jiangsu known for stainless steel and health food, had no previous connection to AI. However, in 2025, a 148-meter-long domestic computing power server production line was established and put into operation here, taking only 180 days from contract signing to production.

The core of this production line consists of two fully domestic chips: the Loongson 3C6000 processor and the Taichi Element T100 AI acceleration card. The Loongson 3C6000 was independently developed from instruction set to microarchitecture. The Taichi Element was derived from the National Supercomputing Center in Wuxi and a team from Tsinghua University, utilizing heterogeneous multi-core architecture.

When running at full capacity, this production line can roll out one server every 5 minutes. The total investment in this production line is 1.1 billion RMB, with an estimated annual output of 100,000 units.

More importantly, the ten-thousand-card cluster composed of these domestic chips has begun to undertake real large-scale model training tasks.

In January 2026, Zhipu AI and Huawei jointly released GLM-Image, the first SOTA image generation model to be fully trained relying on domestic chips. In February, China Telecom's billion-scale "Xingchen" large model completed end-to-end training on a domestically produced ten-thousand-card computing power pool in Lingang, Shanghai.

The significance of these cases is that they prove one thing: domestic chips have transitioned from "usable for inference" to "usable for training." This is a qualitative change. Inference only requires running pre-trained models, with relatively low chip requirements; whereas training involves handling massive data, performing complex gradient calculations and parameter updates, with demands on chip computation power, interconnect bandwidth, and software ecosystem an order of magnitude higher.

The core force undertaking these tasks is Huawei's Ascend series chips. By the end of 2025, the number of developers in the Ascend ecosystem had exceeded 4 million, with over 3,000 partners. Forty-three mainstream industry large models had completed pre-training based on Ascend, over 200 open-source models had been adapted. At the MWC conference on March 2, 2026, Huawei also launched a new generation of computing power base SuperPoD for overseas markets.

The FP16 computing power of Ascend 910B has already caught up with NVIDIA A100. Although the gap still exists, it has changed from unavailable to available, and from available to becoming usable. Ecosystem development cannot wait until the chip is perfect before starting. It must be massively deployed in the usable stage, using real business needs to drive the iteration of chips and software. Bytedance, Tencent, and Baidu aim to import domestically made computing power servers, with a widespread doubling in 2026 compared to the previous year. Ministry of Industry and Information Technology data shows that China's smart computing scale has reached 1590 EFLOPS. In 2026, it is becoming the first year of domestic computing power scale deployment.

American Power Shortage and China's Overseas Expansion

In early 2026, Virginia, which carries a large amount of global data center traffic, suspended the approval of new data center construction projects. Georgia followed suit, with approval suspensions extended to 2027. Illinois and Michigan have also introduced restrictive measures.

According to the International Energy Agency, in 2024, U.S. data centers consumed 183 terawatt-hours of electricity, accounting for about 4% of the national total electricity consumption. By 2030, this number is expected to double to 426TWh, with the share possibly exceeding 12%. Arm's CEO even predicts that by 2030, AI data centers will consume 20% to 25% of the U.S.'s electricity.

The U.S. power grid is already overwhelmed. The PJM grid covering 13 states in the eastern U.S. is facing a 6GW capacity shortage. By 2033, the U.S. as a whole will face a 175GW power capacity gap, equivalent to the electricity consumption of 130 million households. Wholesale power costs in data center-concentrated areas have increased by 267% compared to five years ago.

At the end of computing power lies energy. And in this energy dimension, the gap between China and the U.S. is even greater than in chips, just in the opposite direction.

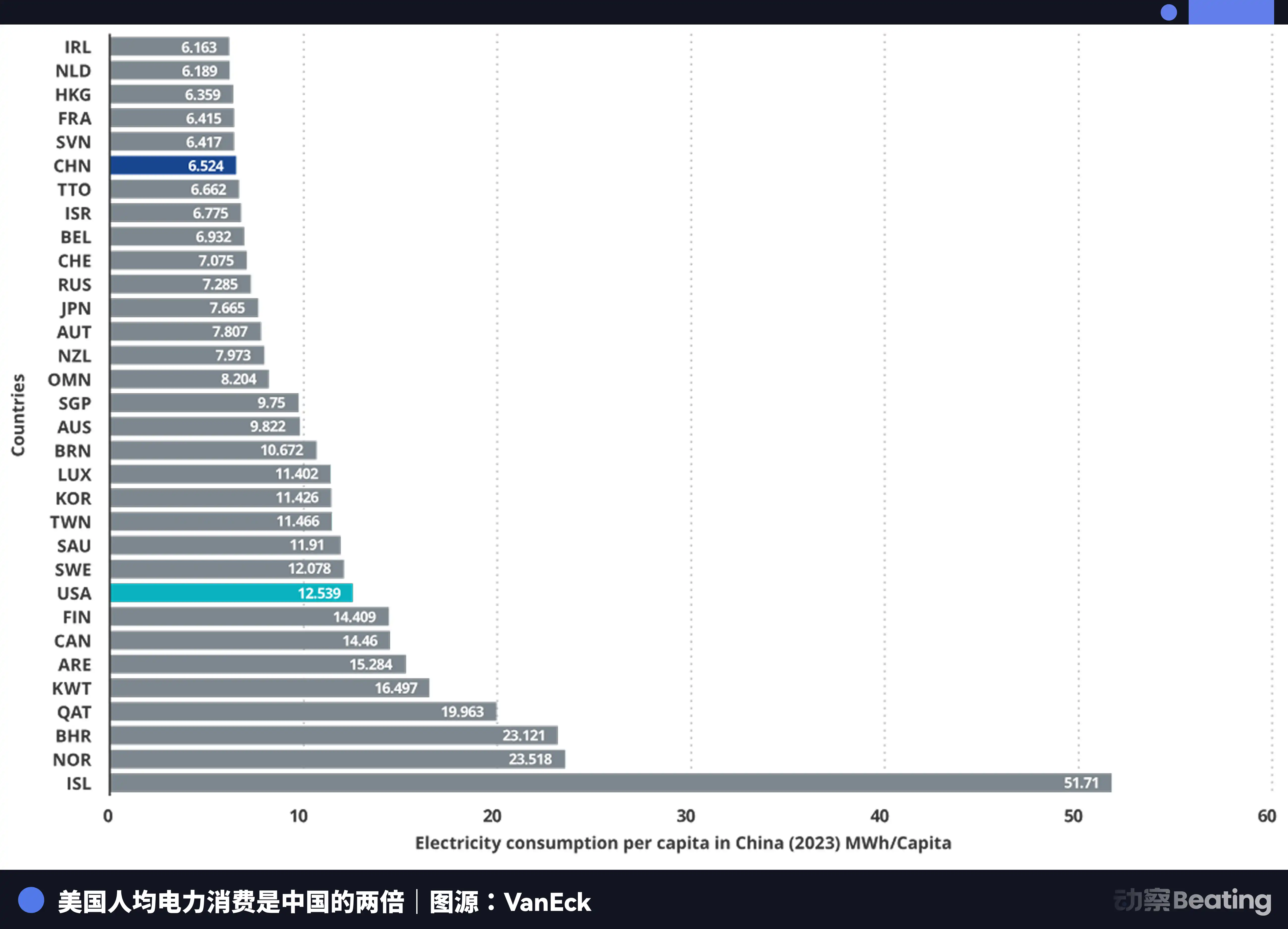

China's annual electricity generation is 10.4 trillion kWh, compared to the U.S.'s 4.2 trillion kWh, making China 2.5 times that of the U.S. More importantly, residential electricity consumption accounts for only 15% of China's total electricity usage, while in the U.S., this proportion is 36%. This means that China has a far larger industrial electricity surplus than the U.S. to invest in computing infrastructure.

In terms of electricity prices, the electricity price in the AI company cluster area in the U.S. ranges from 0.12 to 0.15 USD per kWh, while the industrial electricity price in western China is about 0.03 USD, only a quarter to a fifth of the U.S. price.

China's electricity generation increment has reached 7 times that of the U.S.

Just as the United States was worrying about its electricity supply, China's AI was quietly going global. But this time, what went global was not a product or a factory, but a Token.

Token, the smallest unit for AI model information processing, is becoming a new digital commodity. It is produced in China's computing power factories and transported globally through undersea cables.

DeepSeek's user distribution data tells a compelling story: China accounts for 30.7%, India 13.6%, Indonesia 6.9%, the United States 4.3%, and France 3.2%. It supports 37 languages and is popular in emerging markets like Brazil. Globally, 26,000 companies have opened accounts, and 3,200 institutions have deployed the enterprise version.

By 2025, 58% of new AI startups have integrated DeepSeek into their tech stack. In China, DeepSeek has captured 89% of the market share. In other sanctioned countries, the market share ranges from 40% to 60%.

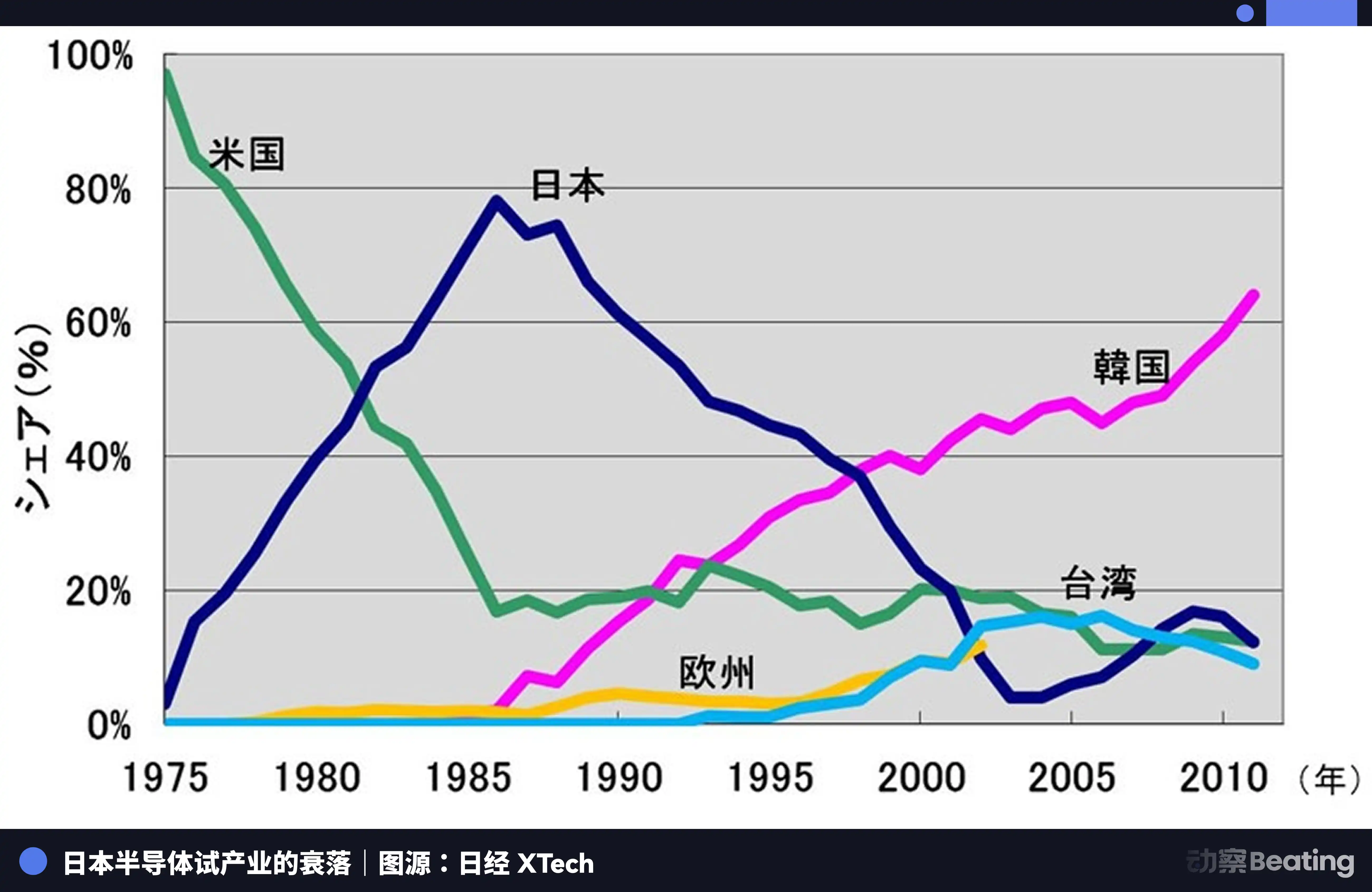

This scene is strikingly similar to another war over industrial autonomy forty years ago.

In 1986, under intense pressure from the United States, the Japanese government signed the "U.S.-Japan Semiconductor Agreement." The core provisions of the agreement had three main points: Japan was required to open its semiconductor market, U.S. chip market share in Japan had to reach 20% or more; Japan was forbidden from exporting semiconductors below cost; a 100% punitive tariff was imposed on $300 million worth of chips exported from Japan. At the same time, the U.S. vetoed Fujitsu's acquisition of Fairchild Semiconductor.

That year, the Japanese semiconductor industry was at its peak. By 1988, Japan controlled 51% of the global semiconductor market share, while the U.S. had only 36.8%. Out of the world's top ten semiconductor companies, Japan held six positions: NEC at second, Toshiba at third, Hitachi at fifth, Fujitsu at seventh, Mitsubishi at eighth, Panasonic at ninth. In 1985, Intel suffered a $173 million loss in the U.S.-Japan semiconductor battle, teetering on the brink of bankruptcy.

But everything changed after the agreement was signed.

Using measures such as the 301 investigation, the U.S. launched a comprehensive suppression of Japanese semiconductor companies. At the same time, it supported Samsung and Hynix in Korea to impact the Japanese market with lower prices. Japan's DRAM market share plummeted from 80% to 10%. By 2017, Japan's IC market share was only 7%. The once dominant giants were either split up, acquired, or quietly exited amid endless losses.

The tragedy of the Japanese semiconductor industry is that it was content to be the best producer in a global division of labor dominated by a single external force, but never thought to build its own independent ecosystem. When the tide ebbed, it found itself with nothing beyond production itself.

Today's Chinese AI industry is standing at a similar yet entirely different crossroads.

Similar in that we also face tremendous pressure from external forces. The three rounds of chip control, escalating layers of barriers, and the towering walls of the CUDA ecosystem.

What is different is that this time, we have chosen a more difficult path. From algorithm-level optimization to the leap of domestic chips from inference to training, to the accumulation of the Ascend ecosystem's 4 million developers, to the penetration of global markets through Token globalization. Each step on this path is building an independent industrial ecosystem that Japan never had.

Epilogue

On February 27, 2026, performance reports from three local AI chip companies were released on the same day.

Cambricon, revenue surged by 453%, achieving annual profit for the first time. Moore Threads, revenue grew by 243%, but with a net loss of 1 billion. Horizon, revenue increased by 121%, with a net loss of nearly 800 million.

Half flame, half seawater.

The flame is the market's extreme thirst. The 95% gap relinquished by Jensen Huang is being gradually filled inch by inch by the revenue figures of these local companies. Regardless of performance or ecosystem, the market needs a second option beyond NVIDIA. This is a rare structural opportunity torn open by geopolitics.

The seawater is the high cost of ecosystem development. Every penny of loss is real money paid to catch up with the CUDA ecosystem. It is investment in research and development, software subsidies, and the manpower cost of engineers deployed to customer sites solving compilation issues one by one. These losses are not due to mismanagement but are the war tax required to build an independent ecosystem.

These three financial reports paint a more honest picture of the reality of this computational power war than any industry report. It is not a triumphant advance but a fierce battlefield engagement fought with bloodshed.

But the form of war has indeed changed. Eight years ago, we discussed the question of "whether we can survive." Today, we discuss the question of "how high a price we must pay to survive."

The price itself is progress.

You may also like

The ten years of Cloud on the Air: From corner coffee to global financial infrastructure

From ByteDance to Financial Freedom: How did "Byte Brother" Leto develop his investment judgment skills to achieve a turnaround of 30 million?

OUSD False Cooperation Controversy? The Credit Game of Stablecoins and Endorsements by Giants

Trump, the best stock trader among U.S. presidents

Q-Day Countdown: Will Quantum Computing End Cryptocurrency?

Selling coins despite a loss of 55 million dollars, the faith in Strategy has reached the interest payment date

The cryptocurrency industry has become a traditional industry

Chip frenzy cooling down? Morgan Stanley's Wilson: Funds are shifting towards AI supercomputing giants like Microsoft and Amazon

$10,000 in TRUMP Token vs. $10,000 in Nasdaq: The "Trump Trade" That Actually Worked in 2026

Morning Report | Vitalik outlines Ethereum's long-term roadmap, Lean Ethereum will become the third major iteration; SK Hynix seeks to attract more AI investors by listing in the U.S

The impact of OUSD on Circle, Tether, and Paxos: not a single negative factor, but a more complex reshaping of competition

Li Feifei's latest long article: When video generation, robots, and NVIDIA all claim to be world models, we need a taxonomy

Blaming the desolation of the cryptocurrency world on the rise of AI is a form of intellectual laziness

Strategy Founder: The Next 10 Years of Bitcoin

Forbes Special Report: Stablecoin cross-border payments are faster now, but not cheaper yet

A valuation of 8 billion dollars, doubling in 8 months! What makes the crypto-friendly bank Erebor Bank stand out?

340 billion valuation: Li Yanhong's largest IPO, a seat in Kunlunxin's shares is hard to come by